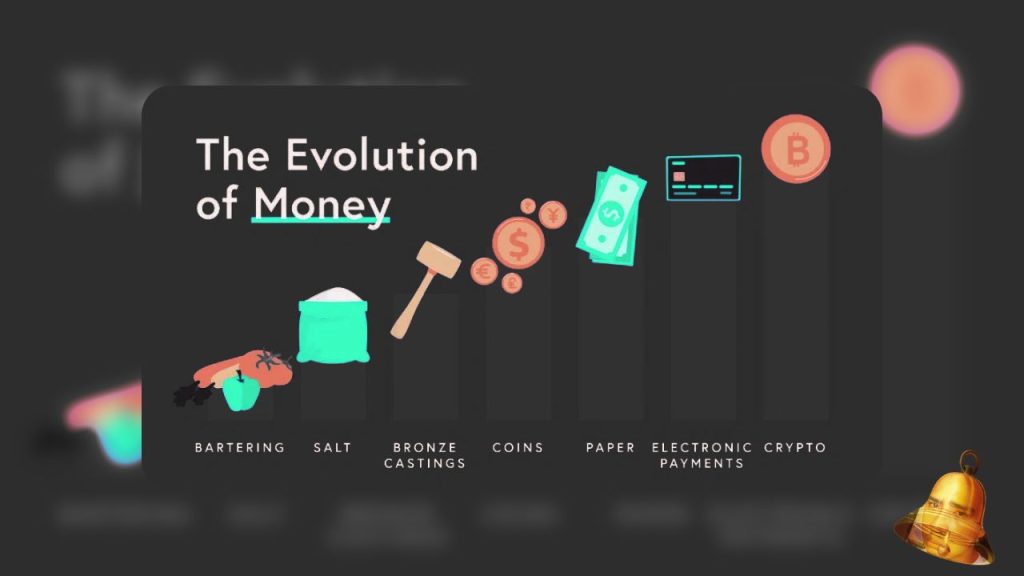

Humans have always needed ways to facilitate the exchange of goods and services. Before money existed, people relied solely on the barter system, directly exchanging one item for another. As civilization progressed, the concept of money emerged as a more efficient medium of exchange than barter. This article examines humanity's long journey in learning about and using money, from barter to the digital era.

Barter System, the Beginning of Human Transactions

In prehistoric times, people exchanged goods such as meat, animal skins, or agricultural products directly. The main obstacle to bartering was the difficulty of finding two parties who mutually needed the goods being offered. Furthermore, the equivalence of the goods' value was often unclear and time-consuming to negotiate. Therefore, humans began searching for solutions that could serve as a more convenient standard of exchange.

The Value of Rare Objects

Around 3,000 BC, in the region of Mesopotamia, now Iraq, certain commodities such as wheat, silver, and copper began to be used as a medium of exchange. The value of these commodities was determined by their scarcity, utility, and widespread acceptance. Although not yet standardized, the use of commodities as a medium of exchange was the precursor to more organized money. Commodity exchange facilitated trade between communities without requiring mutual possession of specific goods.

Money in Number Form

Before the advent of metal coins, the Mesopotamians had developed an accounting system using marks on clay tablets. These 7,000-year-old transaction records demonstrate the use of "money as record" or "money of account." Furthermore, various ancient cultures also used tally sticks, bones marked with counting marks, to record debts and receivables. These traces indicate that the idea of using numbers as a means of measuring value existed long before coins were used.

The Appearance of Metal Coins in Lydia

Around 600 BC, in the region of Lydia (now western Turkey), humans minted the first metal coins from gold and silver. These coins had a standardized weight and metal content, eliminating the need to calculate the value of each commodity in transactions. This facilitated trade, especially across regions. Coins also carried royal symbols or the names of rulers, gaining widespread acceptance and trust across various tribes and cultures.

The Role of the Mesopotamian Shekel

Before Lydian coins, Mesopotamia used the sukuk or shekel as a unit of exchange around 5,000 years ago. The shekel originally measured the weight of silver recorded on accounting plates. Besides facilitating local transactions, the shekel served as a benchmark for intercity debts. The shekel's existence reinforced the idea that money could be a standard of value, not just a tangible object.

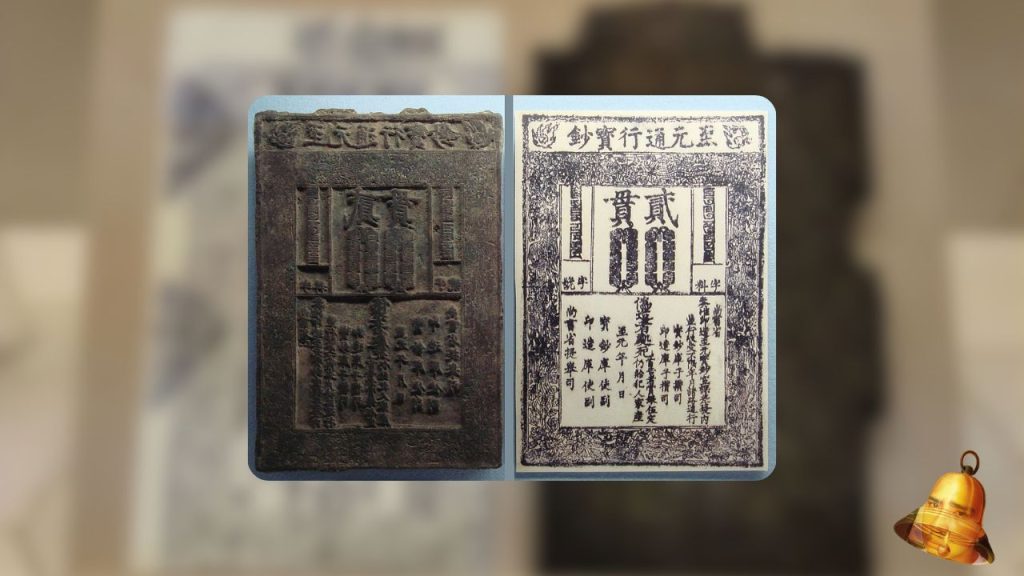

Banknote Innovation

In the 7th century AD, the Tang Dynasty in China created paper money as securities representing the value of metal coins. Initially, paper money was used by merchants to facilitate long-distance transactions, as carrying large amounts of metal coins was risky. Later, the government monopolized the issuance of paper money to strengthen fiscal control. This step marked a significant milestone in the evolution of money from a physical medium to a standardized document.

Shell Money and Other Unique Items

Various ancient cultures also used rare objects such as shells, beads, and precious metals as a medium of exchange. Seashells, for example, were used as money in the Americas and East Asia thousands of years ago due to their uniqueness and difficulty in obtaining them. These objects were considered to have intrinsic value and were accepted in various social ceremonies and trade transactions. The use of unique objects suggests that humans tended to prefer a medium of exchange that was easily identifiable and difficult to counterfeit.

Digital Money and the Modern Era

Entering the 20th century, technology gave birth to credit cards, electronic transfers, and even digital funds. Central banks and financial institutions developed cashless payment systems to increase efficiency. Today, online transactions using fiat currencies and cryptocurrencies are increasingly common. This evolution demonstrates that the concept of money is constantly evolving to meet the needs of the times, but its primary function remains the same: as a medium of exchange, a unit of measure for value, and a store of wealth.

Factors That Accelerate the Development of Money

Several crucial factors accelerated the evolution of money, including:

- Ease of access and transportation of goods

- Growth of intercontinental trade networks

- Advances in printing and communication technology

- Political stability that supports the monopoly of money issuance

Each innovation emerged to overcome the limitations of previous systems and increase the speed and security of transactions.

Conclusion

Humanity's journey with money began with simple barter, evolving into valuable commodities, standardized metal coins, and finally, paper and digital money. Each step was born out of the need to facilitate exchange and objectively measure value. By understanding this long history, we can appreciate how money has shaped civilization and paved the way for the modern global economy.